Most lenders run a single scoring model across the entire book. It was trained once, validated carefully, then frozen, and now it judges a ₹10,000 micro-loan and a ₹5 crore home loan against essentially the same criteria.

That uniformity feels safe. It is consistent, auditable, and easy to govern, but consistency is not correctness, and a yardstick built for the median applicant quietly misreads everyone at the edges.

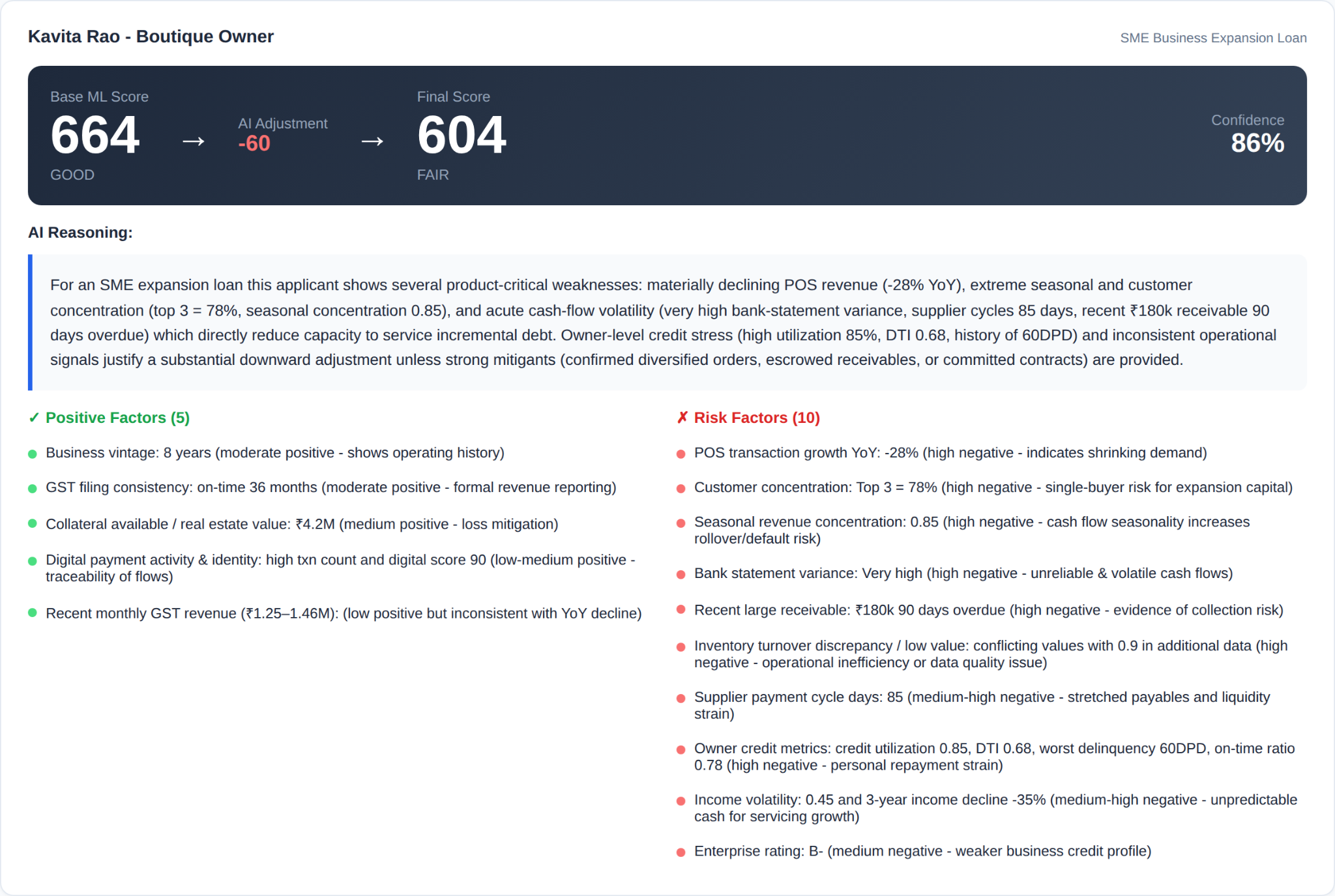

The salaried professional and the self-employed shop owner are not the same risk in different clothes. One is best understood through income stability and repayment history, the other through asset base, revenue trend, and customer concentration. Score them on identical features and you over-penalise the borrower whose strengths your model was never taught to value.

The cost shows up where it is hardest to spot. It is not in the loans that default, but in the good loans you never wrote. A thin-file applicant with strong alternative signals doesn't trigger an alarm; they simply fail to clear a bar designed for someone else, and you never learn what you lost.

Picture how a new product reaches the market today. Credit risk defines the policy, data science sources and engineers the features and retrains the model, validation runs, compliance reviews. Weeks pass before the first application is scored, and the result is yet another fixed model, already frozen against next quarter's reality.

Want to weigh a new signal, say a gig platform rating, GST-filed revenue, or wallet transaction history? The answer is another retraining cycle. A model cannot reason about data it never saw in training. It can only be rebuilt to include it.

None of this reflects a lack of skill. Your risk and data teams are good at what they do. The trouble is that careful manual judgement, applied one model and one retrain at a time, does not scale to the number of products, segments, and data sources a modern lender now has to serve.

The fix is not to throw away your XGBoost model. It is to give it judgement.

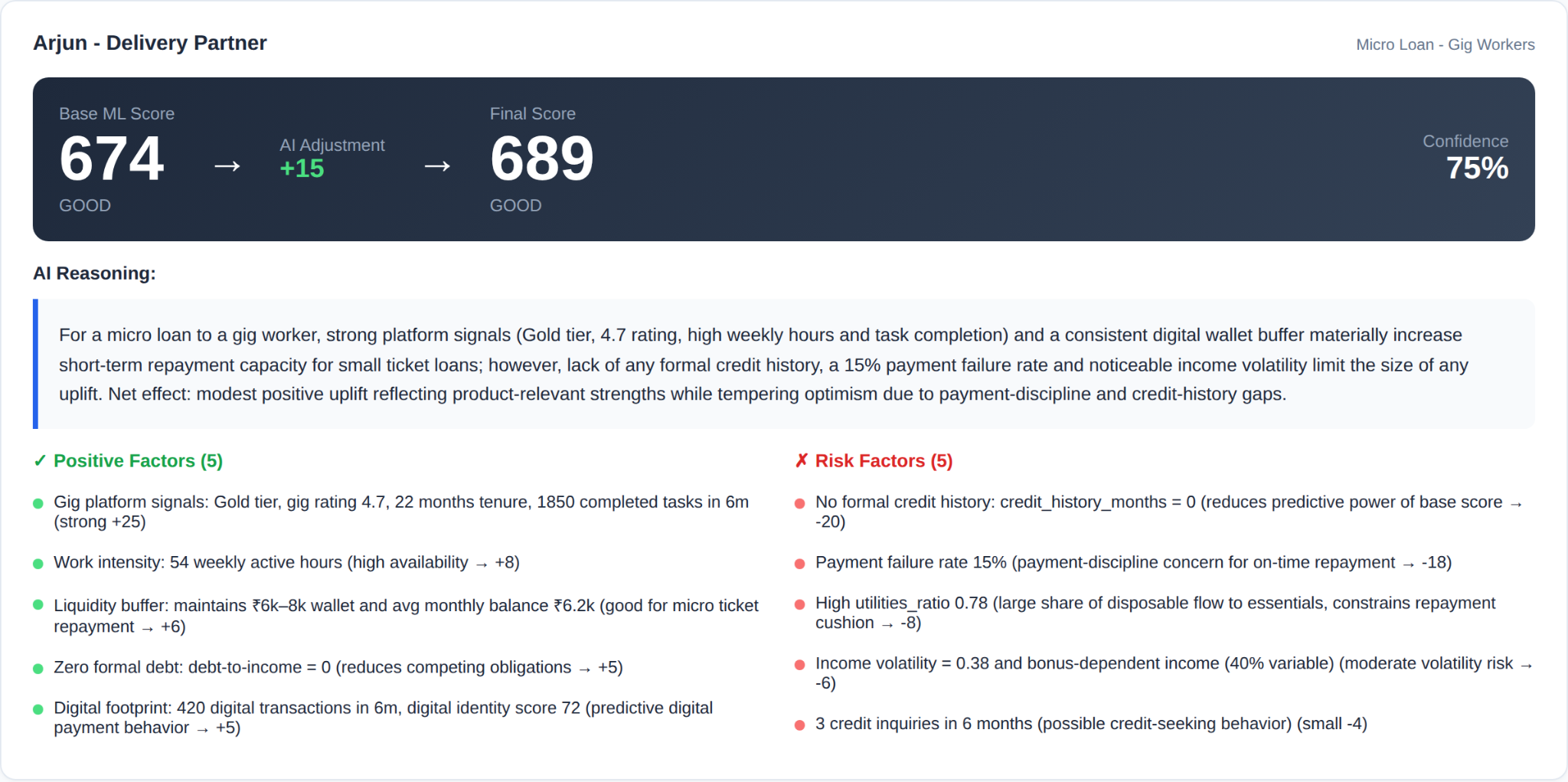

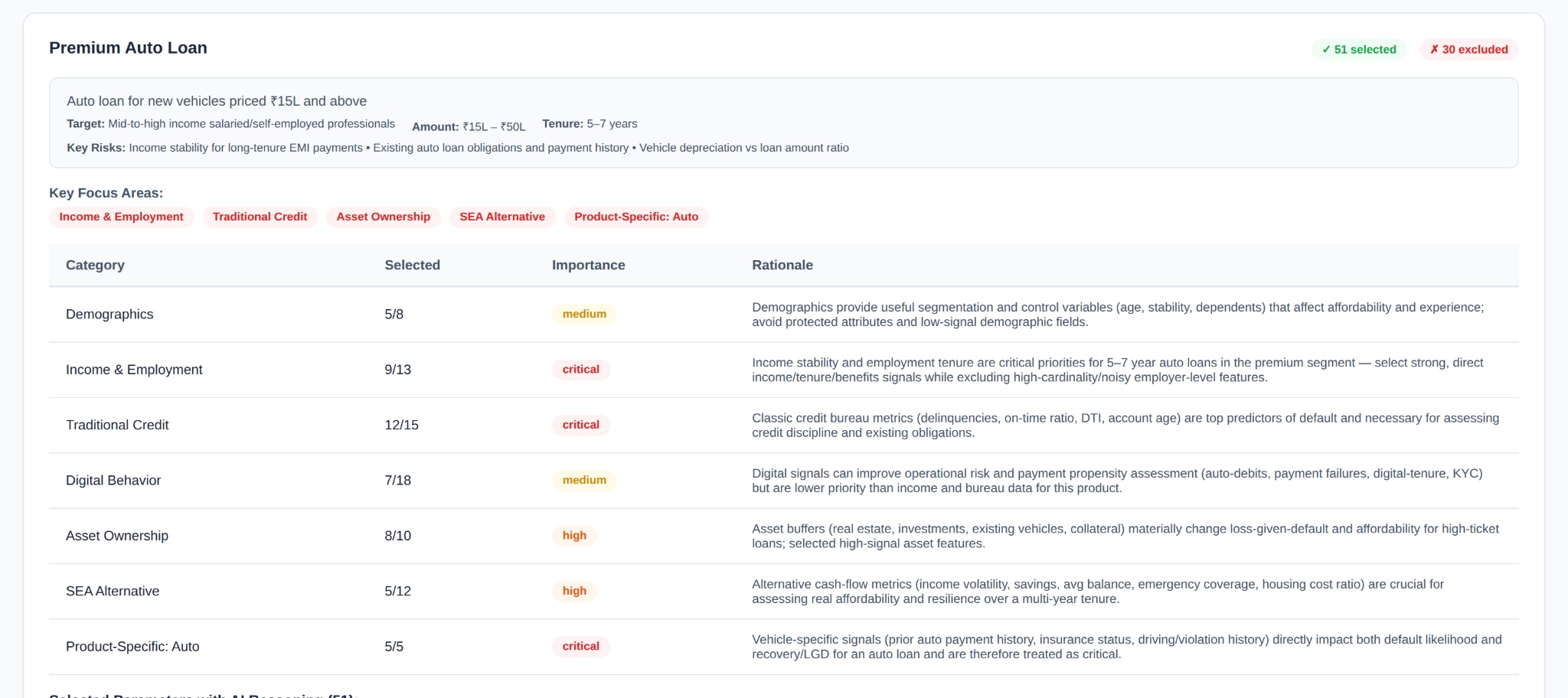

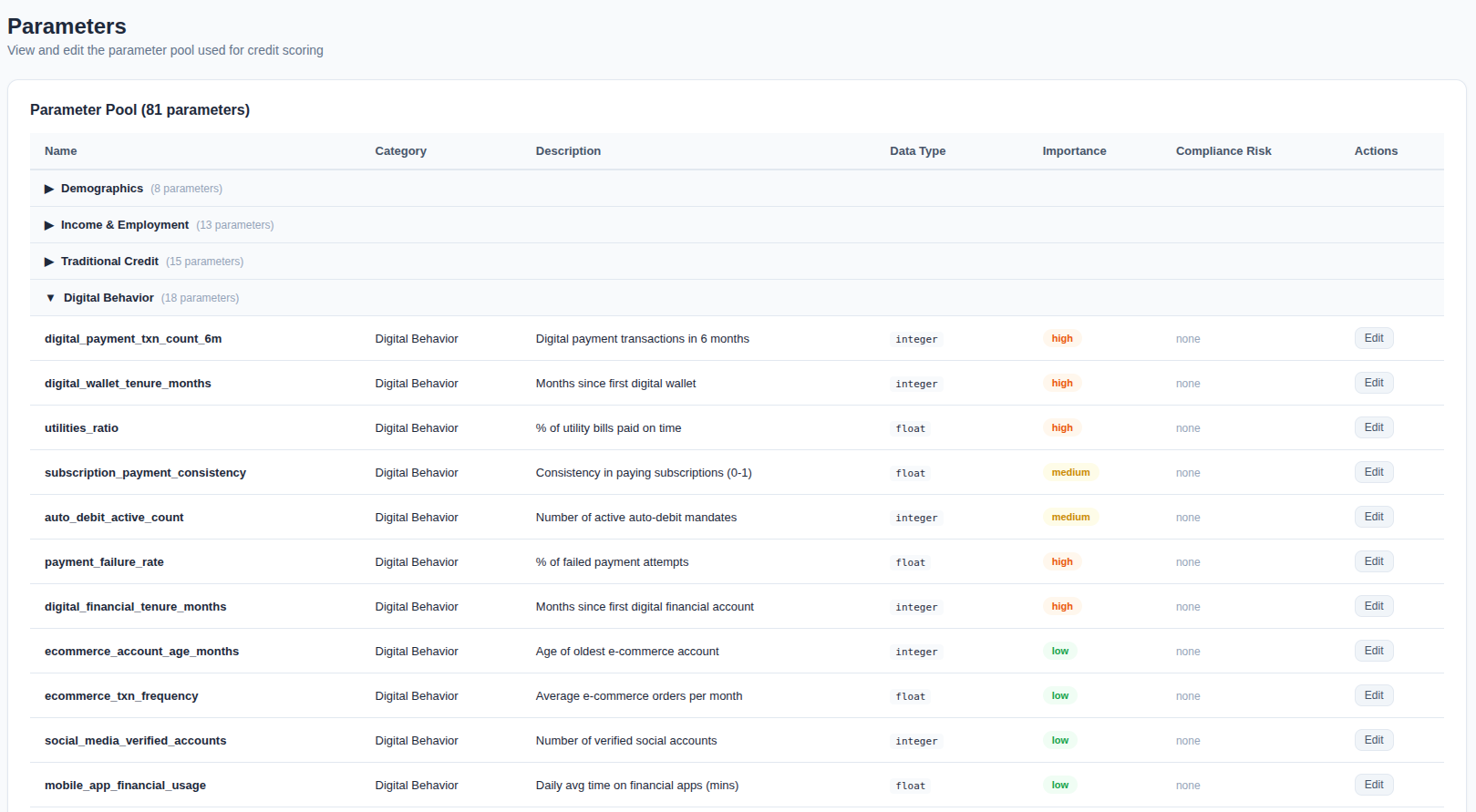

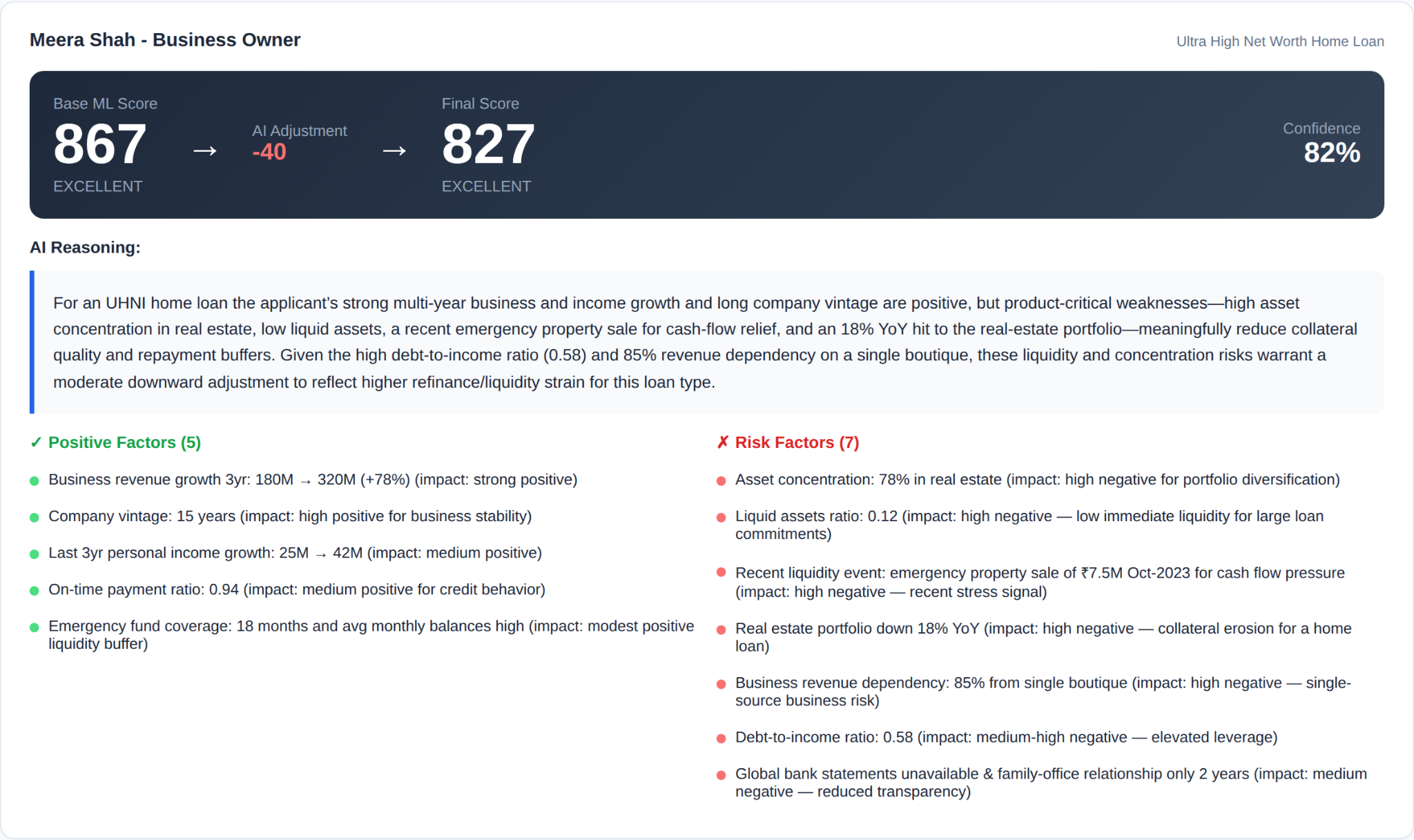

PIPRA's solution adds an AI reasoning layer on top of your existing credit model. For each loan product, the layer selects the relevant subset from a pool of 81 signals across seven categories, with protected attributes automatically excluded. It then takes the model's base score and adjusts it using contextual data the model was never trained on, and every adjustment ships with a plain-language explanation.

The goal is simple to state. Judge each product on the criteria that actually predict its risk, using all the data you already hold, with a defensible reason attached to every score.

Decisioning moves from assumption-led to insight-led. Rather than force every applicant through one fixed lens, the system reasons about which signals matter here, for this product, for this borrower, and tells you why.

The value sits in what the lending business can suddenly do that it couldn't before.

Product-aware from the first application. Each product draws on the signals that fit it. Driving record and income stability for premium auto; platform ratings and payment streaks for gig micro-loans. No separate model for each.

New products arrive in a day rather than a retraining cycle. Define a product in config mode and the AI re-selects from the 81 signals immediately. No frozen model, no weeks of lead time.

Thin-file and informal-income applicants are scored on alternative data, so creditworthy borrowers your current model can't see become approvable. The reasoning that lifts a strong applicant also surfaces real risk, things like customer concentration and cash-flow variance, rather than hiding it.

And every score carries its reasoning plus a compliance-filtered signal trail, which turns the black box into a documented decision a regulator can read.

This does not replace your credit team. It extends their reach.

Your risk experts bring context, policy intent, and accountability. They understand what a number means for the book and the regulator, they decide the appetite, and they own the outcome.

The AI brings speed and consistency. It can weigh dozens of signals per applicant without fatigue or shortcut, doing the reading at scale while your people do the judging at the level that matters. Expert policy, applied consistently to every applicant, with a written rationale your team can inspect and challenge.

Lending is fragmenting faster than fixed models can keep up. Borrowers arrive with gig income, GST filings, and digital footprints instead of clean bureau histories. Product variety is exploding and customers expect decisions in minutes, so a scoring approach that needs weeks to adapt falls further behind every quarter.

Understand each borrower better and the outcomes follow: more good loans approved, real risks seen clearly, and far fewer decisions left undocumented.

What makes this durable is that the engine is signal-agnostic. The reasoning layer doesn't care whether it's reading a gig rating or a GST return, only whether the signal is relevant to the product in front of it. Retarget it from micro-loans to mortgages to SME credit and the framework holds while only the data changes.

That is the real shift. One-size-fits-all, retrain-to-change, black-box scoring gives way to product-aware, instantly adaptable, explainable credit decisioning, built to read the data you already have and confidently approve the customers your current model can't even see.

The AI-augmented credit scoring engine is available for demonstration from Pipra Solutions. If you want to see a walkthrough how it reads alternative data to approve creditworthy thin-file borrowers, surfaces real risk honestly, and attaches a defensible reason to every score we would be glad to connect. Reach out to Pipra Solutions to see what it looks like in practice.