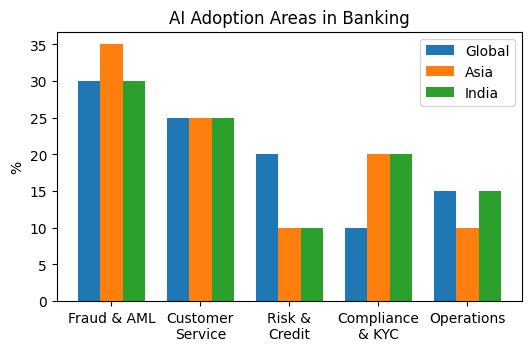

AI adoption in banking is currently concentrated in fraud detection, AML monitoring, customer service, compliance, and operational automation. Global banks are relatively more advanced in credit and risk analytics, while Asian and Indian banks have prioritized fraud prevention and regulatory compliance.

Across India, the Middle East and Asia-Pacific, banks are under unprecedented pressure to modernize. Digital payments, fintech competition, open banking and rising customer expectations are forcing financial institutions to rethink technology strategies. While digital adoption has accelerated, many banks still face structural challenges including legacy systems, fraud, compliance complexity, customer experience gaps and cybersecurity threats.

Many banks continue to operate on core platforms-built decades ago. These systems were not designed for cloud, APIs, mobile-first banking or AI-driven operations.

a. State Bank of India addressed this challenge by building digital capabilities such as YONO while modernizing backend systems incrementally.

Business Benefits: Since its launch, YONO has helped SBI originate over ₹60,000 crore of retail loans digitally, process transaction volumes exceeding ₹10 lakh crore annually, onboard millions of customers at a fraction of traditional acquisition cost and contribute significantly to the bank's record profitability through lower operating costs and higher digital engagement.

b. DBS Bank in Singapore followed a similar transformation journey through cloud adoption and API-based architecture.

The way ahead will involve a change in mindset which will exemplify benefits over integration risks and an incessant desire to adapt.

The explosive growth of digital payments has increased exposure to phishing, account takeover fraud and social-engineering attacks.

a. UPI-related fraud cases. A notable example was the 2021–22 DBS and OCBC SMS phishing scam in Singapore, where cybercriminals impersonated banks through fraudulent messages and diverted thirteen million dollars from customer accounts. The modus operandi was

b. SMS phishing incidents in Singapore highlight the scale of the challenge. Fraudsters sent messages appearing to originate from legitimate bank channels and redirected customers to counterfeit websites where login credentials and OTPs were harvested. Millions of dollars were stolen before the attacks were contained.

The Singapore SMS phishing incidents accelerated investments in AI-powered fraud detection, stronger authentication mechanisms, and real-time transaction monitoring across the banking sector.

Pipra Solutions can help banks strengthen fraud prevention through AI-powered anomaly detection, real-time transaction monitoring, behavioral analytics, risk scoring, and advanced authentication solutions. By leveraging data analytics and intelligent automation, banks can identify suspicious activities faster, reduce fraud losses, improve customer trust, and enhance regulatory compliance.

Banks must navigate increasingly complex requirements around AML, KYC, cybersecurity and data privacy.

a. Global institutions such as HSBC invested heavily in automated compliance and transaction monitoring following regulatory actions. Between 2003 and 2010, AML controls at HSBC were found inadequate, resulting in regulatory action in the United States. HSBC paid approximately US$1.9 billion in fines and settlements in 2012.

Following a US$1.9 billion AML settlement, HSBC invested billions of dollars in compliance modernization, transaction monitoring, and AI-enabled AML controls to strengthen regulatory compliance and reduce future risk exposure.

b. Across India and the Gulf, RegTech solutions are reducing manual effort while improving compliance accuracy. These technologies have reduced customer onboarding times from days to minutes- upto 80%, lowered manual compliance effort by 40–70%, improved compliance accuracy, and enabled banks to manage growing regulatory requirements without proportionally increasing compliance headcount. The result is lower operating costs, faster customer acquisition, reduced regulatory risk, and improved audit readiness.

c. Many Indian banks and NBFCs now use:

Aadhaar-based verification

Video KYC

Automated document validation

Modern customers expect the same convenience from banks that they receive from digital leaders. While leading institutions such as DBS, HDFC Bank, and Emirates NBD's Liv. have demonstrated the value of AI-driven personalization, digital onboarding, and mobile-first banking, many banks across India, the Middle East, and Asia still struggle with fragmented customer data, legacy systems, and limited personalization capabilities.

Pipra Solutions can help bridge this gap by leveraging AI, advanced analytics, customer data platforms, and intelligent automation to create unified customer views, enable hyper-personalized offerings, streamline digital onboarding, and deliver seamless omnichannel experiences. This helps banks improve customer engagement, increase retention, accelerate product adoption, and strengthen long-term customer loyalty.

The Bangladesh Bank SWIFT attack and major data breaches across the financial sector underscore the importance of cybersecurity. Hackers infiltrated the systems of Bangladesh Bank and sent fraudulent payment instructions through the SWIFT international banking network. Fraudulent transfer requests totaled nearly US$951 million. Around US$81 million was lost. This happened due to weak cybersecurity controls and inadequate network segregation coupled with outdated infrastructure.

Banks are open to investing in zero-trust architectures, Security Operations Centers, AI-powered threat detection and continuous monitoring.

Role of Technology providers such as Pipra Solutions is to become strategic partners rather than traditional vendors.

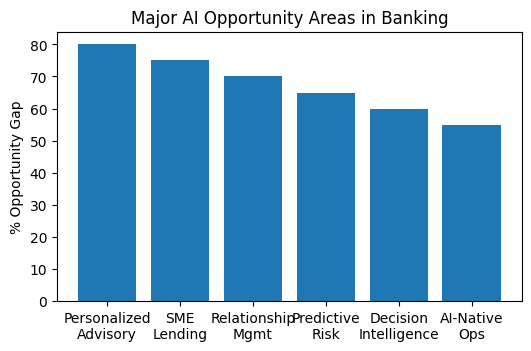

Despite growing AI investments, significant opportunities remain. Personalized financial advisory, SME lending, relationship management, predictive risk analytics, enterprise decision intelligence, and AI-native operations remain underpenetrated across most banking markets. These represent the next phase of banking transformation.

The future of banking in India, MEA and Asia will be shaped by institutions that successfully leverage AI, cloud computing, automation and advanced analytics. The challenge is no longer whether banks should transform, but how quickly they can do so while maintaining trust, security and regulatory compliance.

RBI, BIS, World Bank, IMF, MAS, UAE Central Bank, SAMA, McKinsey, Deloitte, PwC, Accenture, KPMG, DBS Bank Annual Reports, SBI Annual Reports and SWIFT publications.